")

By Christian Hudspeth, CFP(R)

At age 80, my grandma told me one of her proudest achievements was helping fund college for her three grandchildren and four great-grandchildren (I remember as she grinned, counting on both hands and then holding up seven fingers).

Her $10,000 investment in each education account covered four years of college tuition for each of us after 10 to 20 years of growth.

This was not to be money just left as an afterthought for heirs to splurge on something.

It was earmarked as a gift of generosity, intention, and something that served a bigger purpose.

And she enjoyed knowing what her money would go to while she was still alive. She understood as the Irish poet and Nobel Laureate William Butler Yeats eloquently put, “Education is not the filling of a pail but the lighting of a fire.”

Are you inspired? What if there was a way you could gift higher education to each of your grandchildren, born and even not-yet-born?

How to use existing 529 funds to create a future legacy

As we talked about in 3 Smart Ways to Use Leftover 529 Funds, many people we’ve met have tens of thousands of dollars sitting in unused 529 plans leftover from when their kids graduated.

If you or someone you know is in this position, know that recent tax law allows you to roll over 529 funds between relatives without limits, making it possible to build a legacy without expensive and complicated trusts.

As an example, if you have $40,000 in leftover 529 funds and four grandchildren, you could transfer $10,000 into a new 529 plan for each.

Given a 6% inflation-adjusted annual return, $10,000 could grow to roughly $28,500 for each grandchild over an 18-year stretch.

That’s enough to attend at least one year of an in-state public university, or even two years of in-state public university tuition without room and board. Not a bad start.

But there’s a way to create an even larger financial impact for future generations too by creating and funding new 529 plans.

For Your Born Grandchildren

As long as your grandchild has a Social Security Number or ITIN, you may open a 529 plan in their name.

Let’s say you’re married and want to give your grandchildren the gift of future education. Assuming no other gifts were made to a grandchild this year, you and your spouse could open and contribute up to $190,000 to each grandchild’s new 529 plan in 2026 using a technique called “superfunding” which avoids triggering the need to file a gift tax return or using up gift tax exemptions.

For those of you with multi-million dollar estates, it can remove those assets from your estate to help you avoid potential estate taxes too.

There is one catch with superfunding – if the grantor (the person who created the account) were to die within the next five years, say in year four, their gift portion of year five would be added back into their taxable estate. So don’t try this without a trusted financial advisor by your side.

For Your Not-Yet-Born Grandchildren

You can only open a 529 for a living person, so what about members of your family that are yet to be?

For not-yet-born grandchildren, you could open a 529 plan in a future-parents’ name, “superfund” it up to an amount subject to gift tax limits, and then those parents could roll it over as their children (your grandchildren) are born.

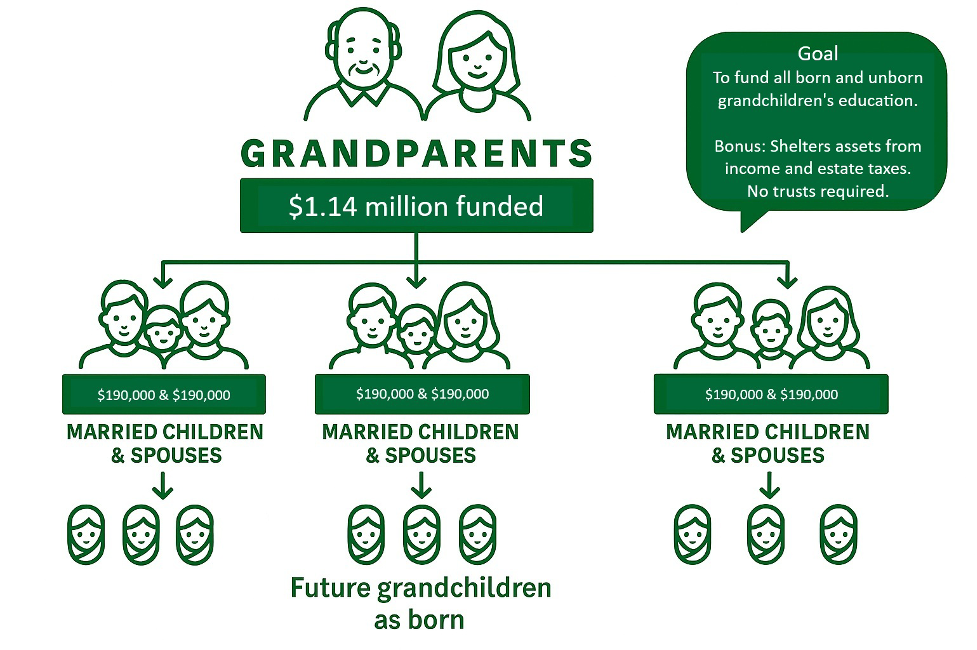

For example, we worked with a married couple to fund six 529 plans with up to $190,000 each – one for each of their three adult children and their three respective spouses (that’s $190,000 X 6 donee parents = $1.14 million gifted to 529 plans).

With a promise from these “donee parents” to honor grandparents’ wishes, they could later open a new 529 plan as each child (their grandchild) is born and rollover/gift to those new 529 plans on their own.

Note: AI helped create this flow chart with edits from the author.

All told, the strategy is set to effectively shelter $1.14 million of grandparents’ wealth from future income taxes and estate taxes.

They also told us it was heart-warming for them to know they’d be funding potentially all of their future grandchildren’s higher education!

And for the grandchildren they blessed? Not only will they get help funding their education, but thanks to the recent “grandparent loophole,” any funds that come out of grandparents’ 529s no longer affect FAFSA or student aid eligibility, so the grandchild may fully receive need-based grants and scholarships.

Looking around the financial corner

I’m humbled and grateful for my grandma’s generous gift of education and how I wouldn’t be here writing this article for you without her!

The lesson it taught me? Most people will react, thinking about the next few years. But if you value thinking proactively about the next generation and planning for your own financial future, you’re in a league of your own and your impact on your family and the world could be profound.

Ready to take the next step and tackle some of your future dreams? Reach out to the author Christian Hudspeth, CFP(R) at chudspeth@fmpwa.com to get the conversation started.

*The information presented here is not specific to any individual’s personal circumstances. FMP Wealth Advisers is not providing investment, tax, legal, or retirement advice or recommendations in this article.

**To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

***These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.